American Rebirth Paper No. 9

This series of papers proposes solutions to American governmental problems that could be addressed by a Constitutional Convention. Please refer to American Rebirth Paper No. 0 to understand additional context of this paper and subsequent papers. American Rebirth Paper No. 6 addressed problems with the Federal budget and proposed solutions to alleviate those problems. This Paper No. 9 will address Federal and state tax reform.

Federal Tax Reform

The way the Federal government raises money today to fund government is dramatically different than what was originally conceived at our founding. Prior to 1913, the government was funded mainly by excise taxes, tariffs and customs duties, and public land sales.

Excise taxes are like sales taxes and were imposed on products such as alcohol, tobacco, and refined sugar. To help pay off debt that had accrued during the Revolution, Congress passed an excise tax on all distilled spirits in 1791, which led to a revolt amongst farmers and distillers in western Pennsylvania (known as the Whiskey Rebellion). The rebellion was a test of George Washington’s presidency – would he allow a rebellious group to go unpunished for not paying the excise tax or would he fulfill his constitutional role to uphold the laws passed? He chose the latter, sending 13,000 militiamen to arrest the 150 rebellious farmers. Eventually, two of the farmers were convicted of treason (later pardoned), and the farmers began to pay the excise taxes.

Public land sales were primarily land sold from territories northwest of the Ohio River. Tariffs on imports have been a source of income throughout our history, but now account for only two percent of the Federal funding.

Income taxes were first imposed soon after the Civil War started, in 1861. The initial rate was set at three percent on all incomes higher than $800 per year. However, Congress acknowledged that there were some problems with this new tax, and no taxes were collected until 1862. By this time, it was clear the Civil War was not going to end quickly, and that additional revenue would be needed to fight the war. Congress passed new excise taxes in 1862 and reformed the income tax law, including creating a two-tiered system where yearly incomes up to $10,000 were taxed at a rate of three percent and higher incomes taxed at five percent. Also, a standard deduction of $600 was enacted and a variety of other deductions (such as rental costs) were permitted. Following the end of the Civil War, the need for Federal revenue declined sharply and most taxes were repealed, including the income tax in 1872.

Congress tried again to enact an income tax in 1894, but this time the new tax was challenged as unconstitutional. In 1895, the Supreme Court ruled that the tax was indeed unconstitutional because it was a direct tax that was not apportioned according to the population of each state as required by Article 1, Section 2 of the Constitution:

“direct Taxes shall be apportioned among the several States which may be included within this Union, according to their respective Numbers”

At the turn of the century, the manufacturing sector in the United States was rapidly growing. From 1880 to 1900, US market share of global manufacturing grew from 15 to 24 percent. Many people were becoming wealthy, and the income gap between the poor and the rich was growing. The progressive ideology during this period was focused on the concept that the government could be a major factor in addressing societal problems, such as class warfare, greed, poverty, racism, and violence.

A feature of this progressive ideology was the idea that taxes should be “progressive,” meaning those that are poor should pay very little while those that are rich should pay a greater percentage. In other words, let us make the rich pay their “fair share.” Excise taxes are not progressive; a poor man and a rich man both pay the same tax on a bottle of whiskey. However, a rich man is more likely to buy a high-end bottle of whiskey, while the poor man will more likely buy a lower quality whiskey. In today’s market, a bottle of Syndicate 58/6 Premium Blended Scotch retails for $390, while a bottle of J&B scotch retails for $31. With an excise tax of 10%, the rich man who buys the Syndicate bottle will pay $39, and the poor man who buys the J&B bottle will pay $3.10. Nevertheless, the non-progressive nature of excise taxes led to groundswell of opinion that income taxes are better than excise taxes because it allows the rich to be taxed at a higher rate.

With this ideology in mind, the Senate and House proposed Senate Joint Resolution 40 (SJR 40), which was then passed by more than two-thirds of the Senate and House on July 2, 1909; SJR 40 proposed a constitutional amendment that allowed the Federal government to impose income taxes directly on all citizens without needing to apportion those taxes based on the population of each state. The tax-the-rich philosophy was an impetus for this amendment as best stated by Representative William Sulzer of New York:

“I have been the constant advocate of an income tax along constitutional lines… I reiterate that through it only…will it ever be possible for the Government to be able to make idle wealth pay its just share of the ever-increasing burdens of taxation.”

The amendment was ratified by the required number of states (75 percent of the 48 states at the time or 36 states) by February 1913; Delaware, Wyoming, and New Mexico were the last three states to ratify. On October 3, 1913, Congress passed the Revenue Act of 1913 that imposed income taxes as was now constitutionally allowed by the 16th Amendment. This act instituted income tax rates beginning at 1 percent of income above $4,000 per year and rising to 7 percent for income more than $500,000 per year. Less than four percent of American families had incomes above $4,000, and due to allowable deductions, less than one percent of the population paid income tax in the first year of the law’s passage.

As we all know, much has changed since 1913 regarding how we are taxed and the amount we are taxed. Many politicians thought that the income tax should be a short-term tax, only used during times of war. Passage of the 16th Amendment, however, along with the continued growth of progressive policies and two world wars have made income taxes permanent. I cannot envision Republicans and Democrats ever managing to agree on tax reform that would eliminate income taxes, but it would be possible if addressed during a Constitutional Convention. I propose we eliminate income taxes and will detail an innovative approach to taxes in this Paper.

As discussed in American Rebirth Paper No. 7 and No. 8, I have proposed eliminating Social Security and Medicare. Although the politicians will tell you the money deducted from your paycheck to fund Social Security and Medicare are not taxes, but “investments” you make to your future retirement, the truth is they are taxes. All the money taken from your paycheck for Social Security and Medicare is spent – it is never invested on your behalf like a 401K. So, along with income taxes, I have proposed to eliminate Social Security and Medicare taxes.

In fiscal year 2021, Federal tax sources included the following:

51% from individual income taxes

31% from Social Security and Medicare

9% from corporate income taxes

2% from customs duties

2% from excise taxes

1% from unemployment insurance

1% from estate and gift taxes

3% from miscellaneous sources

Revenue from the above sources totaled $4.05 trillion versus a total of $6.82 trillion in spending, resulting in a deficit of $2.77 trillion. This paper is about tax reform, but I must point out how absolutely unworthy our government is for allowing these huge deficits. When will it end – does the country need to have another Great Depression? Our politicians are mortgaging our future and the future of our children and grandchildren. Now, back to taxes.

Before I describe an innovative approach to taxes, let’s first identify problems with our current system. First, a very simple question: What is the purpose of taxes? The obvious answer – to raise revenue to fund the operation of government. While this simple question and answer seem very logical, that is not at all what our current tax system is about. Yes, it does raise revenue to fund the government, but the tax code has evolved more to punish some and reward others than it has to efficiently raise revenue. That issue is the primary problem with our tax system. Politicians, in an effort to influence and gain voters, have demonized the rich and reduced the income taxes of low-income individuals such that the top ten percent of wage earners pay 70 percent of the income taxes while 50 percent of wage earners pay less than 15 percent of the income taxes (these percentages vary from year to year with the general trend towards more taxes collected from the rich and less from the low-income). It’s only natural for politicians to curry favor with people that make less money – they are in the majority and it’s easy to stoke the “tax the rich because they’re greedy bastards” trope. They promote divisive rhetoric, pitting the middle class and lower class against those that have succeeded and become wealthy. The wealthy are demonized, despite the obvious benefit these individuals have had on our society. It is the wealthy that creates businesses, invents new products that we all want and love (such as the cell phone), and provides well-paying jobs to millions of Americans. Politicians play to the lesser emotions (primarily envy) of the masses to stoke hatred towards the wealthy while pointing out that it’s only they (the exulted and vastly superior individuals in government) who can make sure you get your “fair share,” and the wealthy pay their “fair share.”

As usual, we can count on politicians for being two-faced hypocrites. While they tout their easy-going approach on income taxes, they portray Social Security and Medicare taxes as “investments” to try and convince wage earners that the 6.2 percent withheld from their paycheck is a good thing.

Politicians also use taxes to reward industries they what to promote (such as electric car companies) while punishing other industries, such as oil and gas companies. In short, the tax system has been modified and massaged based on the influence of lobbyists, environmentalists, and all other manner of organizations that influence politicians, which includes influence in the form of political campaign donations.

The other primary problem with our current system is its complexity and cost. The current tax code is over 70,000 pages long, and as anyone knows that has attempted to read the code, it is often practically impossible to understand and interpret for the average person. As a result, businesses and individuals spend an extraordinary number of hours and dollars to prepare the required forms and pay their taxes.

The IRS collects data from businesses and individuals on the time spent and cost of preparing their taxes. In a study of fiscal year 2009, the IRS estimated that the total cost for businesses was between $92 and 110 billion – about 0.5 percent of GDP. Others have estimated the total yearly cost for businesses and individuals combined is about 1 percent of GDP. I don’t know about you but spending money on filling out forms to pay my taxes is way, way down on the list of things I want to spend money on.

In fiscal year 2019, the IRS had 74,454 employees with a budget of $11.3 billion. The Democrats have been pushing doubling this number of employees with the goal of expanding IRS auditing. If you’ve ever done some work for cash and didn’t report the income, be prepared to face greater scrutiny. The Democrats want to monitor bank accounts that have total yearly deposits of only $600. Obviously, their goal is to go after taxes from everyone, not just the rich.

When Congress considers either a reduction in taxes or an increase, the bills passed are generally complicated and difficult to understand, particularly with increases. The most recent tax cuts passed by the Trump administration did decrease taxes for most Americans, including the middle and lower class, but Democrats spouted rhetoric that the tax cuts only benefited the upper class and very wealthy, leaving many Americans confused or believing the Democrats were correct. In other words, the complexity of the tax system is too often used to score political points, making it difficult to change the tax system.

The complexity of the tax system also lends its hand to targeting of political opponents. If an individual (such as President Trump) is wealthy and has run a large, complicated business, the party in power can attempt to use the Justice Department to smear and, in general, make life miserable for the targeted individual. The goal is not to uncover any crime (while that would be a big bonus, it’s very unlikely to happen as any smart businessman will know that following the law is always right). The goal is typically to feed innuendo and outright rumors to the gullible and complicit media that then write smear pieces on the target while also causing the target to spend inordinate amounts of money defending their business’s tax practices. President Trump is being targeted to show every other successful businessman that their lives would be much more difficult if they attempt to follow in Trump’s footsteps. The politicians only want career politicians in Congress – what a tragedy if most of Congress was made up of ordinary people that have earned a living by working!

Given these problems, how can we reform the way taxes are collected? As discussed in American Rebirth Papers No. 1 and 8, eliminating Social Security and Medicare is proposed, including replacing the current payroll taxes with a retirement fund (instead of Social Security) and Health Savings Accounts (instead of Medicare). Therefore, in this Paper, I will only address reforming the remainder of the tax system, which is primarily composed of individual and business income taxes. The reformed system must achieve the following objectives:

Flatten tax collections such that everyone pays some taxes and the percentage of taxes paid by the upper 50 percent of wage earners is reduced. Currently, the upper 50 percent are responsible for 85 percent of the revenue raised by income taxes. Perhaps this level of responsibility could be reduced to 75 percent.

Eliminate opportunities for politicians to use the tax system for political gain, including rewarding businesses and organizations that curry favor with the politicians and punishing businesses and organizations that have opposing views (or are a convenient scapegoat, such as punishing fossil fuel companies to appease environmentalists).

Simplify the tax system to reduce the size of the IRS and to reduce the cost of paying taxes.

The discussion that follows is intended as a starting point to develop a reformed tax system. I have not collected the necessary data to be able to present a fine-tuned approach; the following ideas are conceptual, and a detailed numerical analysis using economic data will be required to determine taxing rates. However, rates of taxation are presented as ranges to provide a general idea of the concept.

The key features of the proposed tax system are as follows:

Eliminate personal income taxes except for capital gains taxes for some higher income individuals and corporations.

Eliminate business income taxes.

Implement a national sales tax on wholesale and retail goods and services.

Maintain tariffs on imported goods and implement taxes on some exports.

Reduce the rate at which capital gains are taxed.

Implement a tax refund program for low-income individuals that are working at least half-time.

We are all familiar with sales taxes as all but 4 states have sales taxes, ranging from 2.9 percent in Colorado to 7.5 percent in California. In addition to sales taxes on retail goods, 45 states also have sales taxes on a variety of services. Some states have a short list of services that are taxed, some have a short list of services that are exempt from taxes, and some tax all services. I believe a federal sales tax would range between 10 and 20 percent. Keeping in mind the goal of eliminating political favoritism and providing some relief to low-income individuals, the following features are proposed for federal sales taxes:

With a few exceptions (identified below), all goods are taxed at the same rate. A toy boat is taxed at the same rate as a mega-yacht.

Some goods and services are exempt from taxation:

a. Except for real estate and investment products (such as rare coins, rare paintings, collectibles), all used goods are not taxed. Generally, anything that is rising in value over time is considered an investment product. Investment products and real estate are taxed as capital gains with no sales tax used on sales.

b. Raw food products, such as milk, eggs, potatoes, vegetables, fruit, rice, flour, sugar, fish, and meat, are not taxed. Once a product is processed it becomes taxable. For example, ice cream is taxable, but raw cream is not. Seasoned meat is taxable, but raw meat is not. A box of macaroni and cheese that is cooked at home is taxable, but uncooked pasta is not.

c. Bulk raw materials used in the United States for manufacturing materials are not taxed. For example, iron ore used to make steel, natural gas used to make fertilizer, and crude oil refined to make gasoline are not taxed. Natural gas that is used for power production is not taxed, but natural gas sold direct to consumers is taxed. Power that is produced by natural gas is taxed. These same bulk materials are taxed if they are exported.

d. Healthcare services are not taxed.

e. All insurance purchases are not taxed.

f. Rental payments for housing are not taxed, but home occupancy assessments (HOAs) are.

g. Tuition is not taxed.

h. Federal and State purchases of goods and services are not taxed.

3. Some goods may have an increased (but never decreased) rate of taxation for special reasons. For example, gasoline could be taxed at a higher rate with the increased tax being used to fund maintenance of and improvements to the interstate highway system. If an additional tax is applied, the added revenue must have a stated purpose.

4. Except for bulk materials used in manufacturing new materials, materials purchased by businesses (either through wholesale or retail outlets) are taxed.

5. Utilities, including water, sewer, power, natural gas and propane, are taxed.

6. In situations where a company subcontracts services, the sales tax is only applied to the amount invoiced to the contract holder. For example, if a building contractor is building a house and pays a subcontractor to do electrical work, the invoice will include the electrical subcontractor’s invoiced amount plus the sales tax applied to that amount. In other words, the work done by the electrical subcontractor is taxed only once.

7. For some items, a set amount of tax per unit of item sold may be used instead of a percentage. For example, a $0.25 tax on each gallon of gasoline may be imposed in lieu of a sales tax based on percentage. However, use of taxes in this manner shall be restricted to only those items that are commodities, where there is no significant difference in functionality and quality across multiple suppliers. In addition to gasoline, other items that might fall into this category include electricity and natural gas.

The primary argument against a sales tax is that it isn’t progressive such that the poor pay too much and the rich pay too little. This argument is put forward by politicians because they do not want to give up the power they wield by being able to manipulate who pays income taxes. The truth is that those with more income will spend more. Based on Department of Labor data, Table 1 shows average yearly consumer spending as a function of income for year 2020. These data characterize the spending of the 128.5 million households in the United States.

Most of the spending categories are straightforward, but some need additional context, including the following:

Housing: Includes rental payments and interest payments on mortgages and home equity loans but does not include payments on the loan principle. Includes utilities, home maintenance services, and purchase of household items such as appliances and furniture.

Insurance and pensions: Pensions are investments in securities (stocks, bonds, etc.) that are intended for retirement income (or additional income while still working).

Cash contributions: Includes alimony and child support payments, care of students away from home, and contributions to charities and other organizations.

Additional information regarding the information shown in Table 1 can be found at: Consumer Expenditures Survey Glossary (bls.gov).

To assess how a sales tax might work, the following exercise was done using the spending amounts shown in Table 1:

A 5 percent effective tax rate was applied to the housing category. This assumes that most of the spending, including rent and interest payments on loans, is not taxed and that the taxable items are taxed at a rate of 15 percent. In other words, two-thirds of the spending is not taxed, and one-third is taxed at 15 percent.

No sales taxes were applied to the insurance and pensions, healthcare, and cash contributions categories.

A 14 percent effective tax rate was applied to the food category. This assumes a 15 percent sales tax with some food (raw food products, such as milk and eggs) being exempted from taxes, resulting in a net sales tax of 14 percent for all food purchases.

A 15 percent sales tax was applied to all other categories.

Adjustments in the tax rates across income quartiles were not made for the purposes of this exercise. This assumption likely underestimates the taxes paid by higher income households and overestimates taxes paid by lower income households. For example, the lowest income households likely spend nearly all their housing cost on rents. If they purchase used appliances and furniture, they will not pay sales tax (used items are exempt from taxation). Higher income households, on the other hand, may have no interest payments or rents, may have multiple homes, and are more likely to purchase new appliances and furniture that are taxable.

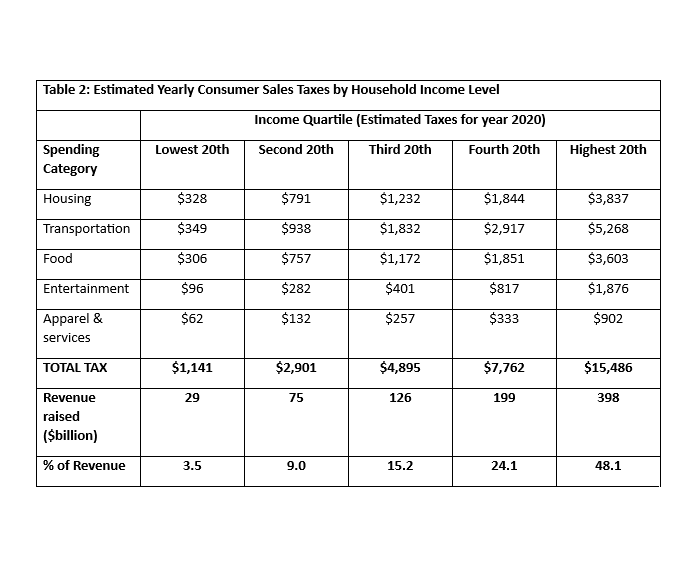

Table 2 shows the sales tax that would have been paid in year 2020 given the above assumptions and the spending amounts shown in Table 1. Given the total number of households of 128.5 million, each quartile represents 25.7 million households. Multiplying the number of households by the total tax provides an estimate of the revenue raised for each quartile. Total estimated revenue for this exercise is $827 billion. In comparison, in 2021 individual income taxes raised revenue of $2 trillion. Since the sales tax is replacing the income tax, does the total of $827 billion estimated by this exercise suggest the sales tax rates are too low? It might, but another major source of revenue (which is included in the $2 trillion revenue for 2021) is capital gains taxes (I’ll discuss a modified approach to capital gains following this discussion of sales taxes).

The percentage of sales taxes paid is shown for each income quartile. Surprisingly, the percentage paid by the top 50 percent is about 80%. In comparison, the top 50 percent of individual income taxes paid is a bit more – 85 percent. While this sales tax approach has flattened the taxes paid by a small amount, it is still quite progressive. Given that the higher income households are more likely to pay capital gains taxes while lower income may pay no capital gains taxes, the combination of sales taxes and capital gains taxes will likely result in a tax burden that is similar to our current system.

I have a couple of final thoughts on sales taxes before I move on to capital gains taxes. First, sales taxes are visible to everyone, and everyone must pay taxes. If the politicians increase taxes, it is readily apparent to everyone because the taxes are shown on every sales receipt. Unlike the current tax system, people in the lower income levels will be paying taxes, and therefore, will be more concerned with attempts to raise taxes.

Finally, as mentioned in the list of items to be included in the tax program, households in the lower income levels will be able to get tax refunds, provided they are working at least half-time. This program is similar to the Earned Income Credit (EIC) currently used for income taxes, where working, low-income people have tax credits (because of EIC) greater than their tax payments, resulting in being paid by the government (i.e. a negative income tax). I’ll be addressing welfare reform in another American Rebirth Paper. The primary feature of the proposed plan will be to eliminate all welfare programs and replace it with payments through a program like the EIC.

Now, on to capital gains taxes. Many economists are in favor of no capital gains taxes at all because taxes on capital gains reduces the availability of capital to fund new ventures. With fewer new start-ups and investments in business ventures, fewer new jobs are created. A billion dollars in the hands of a venture capitalist versus in the hands of government will be more beneficial to society as the venture capitalist is more likely to create jobs. Our goal as a society should be to maximum the number of people working and minimize the number of people requiring government assistance. The best way to achieve this goal is to create new jobs while providing incentives for people to work and disincentives for people to live off government largesse. Therefore, in my opinion, capital gains taxes need to be a low percentage. As a starting point, the following approach is suggested:

No capital gains taxes for yearly gains less than $200,000.

5 percent taxes for yearly gains between $200,000 and $1 million.

10 percent taxes for yearly gains above $1 million.

No capital gains taxes for an individual’s primary home. All other real estate is taxed.

Limits given above are adjusted for inflation on a yearly basis.

Withdrawals from 401K and for other retirement plans (such as the new plan to replace Social Security described in American Rebirth Paper No. 7) are also taxed but gains are adjusted for inflation. Capital gains for investments that are not in a 401K are not adjusted for inflation. Note that because income taxes are eliminated, the current tax-free attribute for contributions to a 401K plan is no longer of any benefit. Also, in the current system withdrawals from a 401K are taxed as income. With elimination of income taxes, those withdrawals are now taxed as capital gains.

Withdrawals from Health Savings Accounts (HSAs) are not taxed.

Some Federal and State bonds may be issued that are not taxed.

One aspect of the proposed replacements for Social Security (see American Rebirth Paper No. 7) and Medicare (American Rebirth Paper No. 8) will impact capital gains. Both new plans will involve funding of individual accounts. Instead of sending part of your paycheck to the government, you will instead have part of your paycheck sent to a privately run investment fund, like a 401K. In year 2021, 31 percent of the tax revenues were from Social Security and Medicare payroll taxes. Thirty-one percent of the total tax revenue of $4.05 trillion is $1.26 trillion. With the new plans, most of this money will be invested in stocks. Since these plans are setting aside money for retirement years, a lot of the money invested will be held in stocks for decades. Currently, the total value of all stocks in the United States is about $50 trillion. If $1 trillion or more per year flows into the stock market, it’s common sense to conclude that stock values will be driven up by the demand imposed by these new retirement plans. As a result, individuals with very large stock holdings (such as Elon Musk) will tend to have their wealth increase simply because of demand for stock they own. While I do agree that having low capital gains taxes makes sense in terms of making capital available for new investments that create new businesses (and along with it new jobs), it seems fair that very wealthy individuals should return some of the gains they make due to the increased money flowing into the stock market.

Another advantage of sales taxes and capital gains taxes: stimulation of the economy is best done through tax cuts. Stimulating the economy by tax cuts has been proven to be effective. The typical leftist approach, on the other hand, is to take money from taxpayers and then give it away in an effort to stimulate the economy. This is an inefficient way to give more money to consumers. In fact, it takes money from consumers and gives it back. At best, it’s a wash. At worst, the government borrows money (instead of taking taxpayer money) and then gives it out based on favoritism. Government handouts with borrowed money (which is borrowed from future taxpayers – it’s not free!) are generally very complicated because the politicians work overtime to delegate how the money is doled out. As a result, rampant fraud and misuse of funds frequently happens. A tax cut is a simple way to leave more money in the hands of consumers. They spend more and thus stimulate the economy. To make things simple, the revisions to the constitution that will be made will stipulate that any tax cut is done across-the-board to eliminate political shenanigans. For example, if the federal sales tax is 15 percent, the tax cut would reduce the tax to 14 percent, perhaps for a temporary period of a year. If the sales tax is raising $1 trillion in revenue, a reduction of 1 percent (from 15 to 14) would provide a $67 billion in stimulus. A sales tax reduction to 10 percent from 15 percent would provide a stimulus of $335 billion.

State Tax Reform

Each state currently uses a variety of methods to raise revenue, including sales taxes, property taxes, and income taxes. In the proposed reformed system, states shall be prevented from imposing income taxes and capital gains taxes. While both federal and states will be able to impose sales taxes, only the federal government shall be able to collect capital gains taxes, and only the states shall be able to collect property taxes. A few states have a business and occupation tax; in the reformed plan, this type of tax shall not be allowed. However, businesses will have to pay property taxes.

In addition to paying property taxes, negotiating one-time payments from businesses and developers that wish to build new facilities in a state shall be allowed. The purpose of these payments is to cover costs that the state may incur to support the new facilities. For example, if a business wants to build a new factory in the state, and it can be shown (most likely through an Environmental Impact Study) that improvements to the roadways are needed to support traffic to and from the factory, then the state can require the company to provide some funding to support upgrades to the roadway system. These payments are only allowed if the funding is directly connected to actual improvements that will be made. The state cannot take money from a company and then spend it on whatever they chose – it must be spent as agreed to by the company and the state.

In closing this Paper, I want to reiterate that the intent of this Paper is to present concepts for a reformed tax system. Obviously, given the amount of money involved and the vast expanse of the American economy, settling on the final approach will require extensive economic analysis. Constitutional revisions would outline taxes that are allowed (for federal and state governments) and taxes that are not allowed (primarily elimination of income taxes) and would also stipulate specific rules that must be followed in implementing taxes. The details of the tax code will need to be passed by Congress.